A Quarterly Publication from Wayne Barnett Software

Volume 100, 1st Quarter 2026

The BSA Examiner is a quarterly newsletter published by Wayne Barnett Software. If you have a question to ask or a story to tell (we promise anonymity), please call us at 469-464-1902.

Case #1—Whose money is it?

The Case:

Mr. Harper spent his whole life in a small farming town. He never married and had no children—just a modest white house, an aging pickup, and a reputation for being frugal.

What most people didn’t know was that Mr. Harper kept a safe deposit box at the bank containing savings bonds, inherited gold coins, and a thick envelope of cash he didn’t trust in an account.

About three months before he passed, Mr. Harper added his recent acquaintance, Linda, to his safe deposit box lease. She had been helping him after he broke his hip—driving him to appointments, picking up prescriptions, and buying groceries. On several occasions, Linda accompanied Mr. Harper to the bank and saw the contents of the safe deposit box.

A few months after adding Linda to the lease, Mr. Harper passed. Two days later, Linda went to the bank to claim what she believed was hers.

The banker, who had known Mr. Harper for years, explained that being a co-lessee provided access to the box—but not ownership of its contents. Linda insisted Mr. Harper had intended for her to have what was inside.

Under Mississippi law, a bank may allow limited access to a safe deposit box after death, typically to inventory contents and retrieve documents such as a will. Ownership of the contents, however, is determined through the estate.

There was no written gift, no transfer documentation, and no payable-on-death designation. When the executor was appointed, the contents—five savings bonds and approximately $80,000 in cash and coins—were inventoried and treated as estate property.

In the end, the court ruled that the contents passed through probate like everything else.

Clear process protects everyone involved:

Situations like this highlight the importance of consistent procedures and clear distinctions between access and ownership. Bank staff followed established processes—verifying documentation, applying state law, and ensuring proper handling of estate assets.

These are not always easy conversations, but they are necessary ones. When handled correctly, they protect the institution, the estate, and all parties involved.

Case #2—Trick out my truck—or trick me?

The Case:

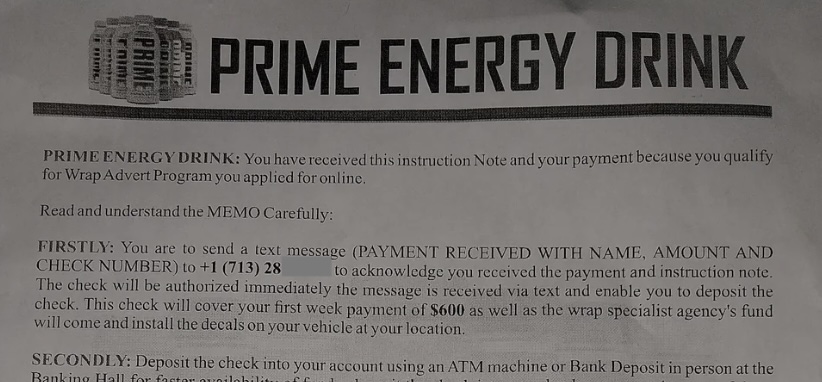

Marcus nearly ignored the text: “We’re launching a new sports drink campaign and will pay you $600 a week to wrap your truck with our logo. Interested?”

Money had been tight, and the offer seemed simple enough. After responding, he was told he had been “selected” and would receive payment immediately to get started.

The next day, Marcus received a check for $3,200. Instructions were to deposit the check, keep $600 as his first week’s pay, and send the remaining $2,600 to a certified installer.

It felt unusual, but the explanation sounded reasonable—“a single promotional check to avoid delays.”

Marcus deposited the check. The next morning, the funds appeared available in his account. Reassured, he sent $2,600 to the installer using Zelle.

Then the installer stopped responding.

Three days later, the bank contacted Marcus. The check had been returned as counterfeit, and the deposit was reversed. The $2,600 he sent was gone—and now he owed the bank.

His truck remained exactly as it had been before. Unwrapped, unpaid, and suddenly very expensive.

Why this scam works:

This type of fraud plays on timing and perception:

- The check appears legitimate

- Funds show as “available” before final settlement

- The request creates urgency

- The victim is asked to move money quickly

By the time the check is returned, the funds sent are already unrecoverable.

Practical takeaway for banks and customers:

As fraud tactics evolve—from safe deposit misunderstandings to modern payment scams—awareness remains the strongest line of defense.

Encourage customers to:

- Question unexpected payment offers

- Avoid sending funds tied to deposited checks

- Verify legitimacy before acting

For the latest scam alerts, visit: https://consumer.ftc.gov/

If you like the commonsense stories and helpful guidance we share in our newsletters, you’ll love our easy-to-use software. We are Wayne Barnett Software.

We’re not a big company, but our products compare nicely with Verafin, Abrigo and the others.

You can contact us at rrigdon@barnettsoftware.com or 469-464-1902. Thanks for reading our newsletter.